Context and Background

Fampay App India represents a relatively new category within the country’s financial technology ecosystem, specifically designed for teenagers and young users who traditionally fall outside the scope of formal banking systems. As digital payments become increasingly integrated into everyday life, access to financial tools is no longer limited to adults with bank accounts. Instead, there is growing demand for platforms that introduce financial participation at an earlier stage.

In India, where regulatory frameworks around minors and banking are clearly defined, this presents both an opportunity and a constraint. Traditional banking infrastructure does not easily accommodate independent financial access for teenagers, creating a gap that platforms like Fampay App India attempt to address.

Rather than functioning as a conventional bank, Fampay App India operates as a prepaid and controlled financial environment. It enables younger users to engage with digital payments, budgeting, and spending within defined limits, often under parental oversight. This approach reflects a broader shift toward financial inclusion that extends beyond access to accounts and into early financial literacy and controlled autonomy.

Fampay App India: Structural Design and Platform Logic

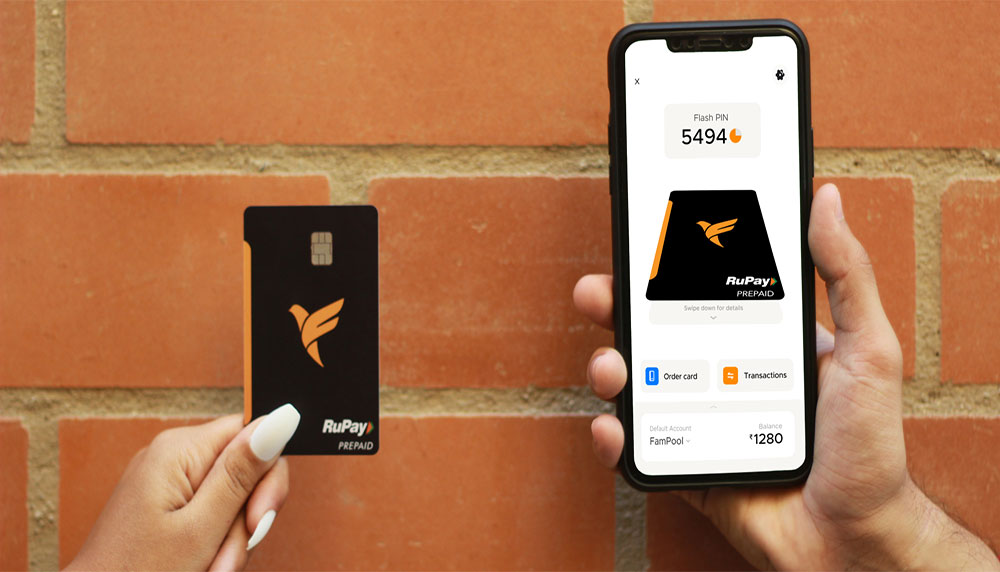

Fampay App India is structured around a prepaid wallet system combined with a card-based interface, often referred to as a numberless card. This design is intended to simplify usage while reducing risks associated with traditional card details such as visible numbers and CVV codes.

The platform operates within a semi-closed financial loop. Users can load funds into the app, typically with parental involvement, and then use those funds for digital transactions. This structure ensures that spending is limited to available balances, eliminating the possibility of credit-based debt.

A key aspect of the platform’s logic is controlled independence. Teenagers are given the ability to make payments and manage money, but within boundaries that can be monitored or influenced by guardians. This creates a hybrid model that balances autonomy with oversight.

However, this structure also limits functionality compared to full-service banking platforms. Users do not have access to traditional banking features such as interest-bearing accounts, loans, or independent financial instruments.

User Experience and Accessibility

The interface of Fampay App India is designed to appeal to younger audiences, with a focus on simplicity, visual clarity, and ease of navigation. The onboarding process is streamlined, reducing friction for first-time users.

The app emphasizes intuitive interaction, allowing users to quickly understand how to load funds, make payments, and track spending. This is particularly important for users who may be engaging with financial tools for the first time.

From a performance perspective, the platform is optimized for mobile usage, which aligns with the behavior of its target demographic. Transactions are generally fast, and the interface is responsive across different devices.

However, the design prioritizes simplicity over depth. Advanced financial tools, analytics, and customization options are limited. While this is appropriate for the target audience, it may restrict long-term engagement as users grow more financially experienced.

Financial Literacy and Behavioral Impact

One of the more significant aspects of Fampay App India is its potential role in shaping financial behavior. By introducing users to digital payments at an early stage, the platform contributes to the development of basic financial habits.

Users learn to:

- Manage limited balances

- Track spending patterns

- Understand digital transactions

- Make independent purchase decisions

This early exposure can support financial literacy, particularly in a digital-first economy. However, the extent of this impact depends on how the platform integrates educational elements into its design.

Without structured guidance or learning tools, users may engage with the platform primarily as a payment mechanism rather than a financial learning environment.

Security Framework and Risk Management

Security is a central consideration for any financial platform, particularly one targeting younger users. Fampay App India incorporates several features designed to reduce risk, including prepaid limits and card anonymization.

The numberless card system reduces the exposure of sensitive information, which can mitigate certain types of fraud. Additionally, the prepaid structure ensures that losses are limited to available balances rather than extending into credit.

Parental involvement also acts as an additional layer of oversight. Guardians can monitor or influence financial activity, adding a level of control that is not typically present in adult financial systems.

However, security is not solely a technical issue. User awareness and behavior play a critical role. Ensuring that young users understand safe digital practices is essential for maintaining a secure environment.

Economic Model and Market Positioning

Fampay App India operates within a competitive fintech landscape, where differentiation is often driven by target audience and use case. By focusing specifically on teenagers, the platform occupies a niche segment that is relatively underserved.

Revenue generation may involve transaction fees, partnerships, or value-added services. Unlike traditional banking models, the platform’s economic structure is closely tied to user activity rather than long-term financial products.

This positioning allows Fampay App India to capture a growing user base, but it also raises questions about scalability. As users transition into adulthood, the platform must either evolve its offerings or risk losing relevance.

Regulatory Considerations

Operating in the financial sector requires adherence to regulatory frameworks, particularly when minors are involved. Fampay App India must navigate these constraints while maintaining usability.

The platform’s prepaid structure aligns with regulatory requirements by avoiding direct issuance of bank accounts to minors. However, changes in regulation or increased scrutiny could impact how such platforms operate in the future.

Strengths and Positive Attributes

Fampay App India’s primary strength lies in its focus on a clearly defined user segment. By designing a platform specifically for teenagers, it addresses a gap in the financial ecosystem. Its prepaid model reduces financial risk, while its user-friendly interface enhances accessibility. The platform also contributes to early financial exposure, which can support long-term financial literacy.

Constraints and Areas of Concern

The platform’s limited functionality compared to full-service banking systems may restrict long-term engagement. Dependence on parental involvement can reduce user autonomy. Financial education features are not deeply integrated, which may limit its impact beyond basic transactions. Additionally, competition within the fintech space continues to increase, which could affect market positioning.

Closing Observations

Fampay App India reflects a broader shift toward inclusive and age-specific financial platforms. By introducing controlled digital payments to younger users, it expands the boundaries of financial participation.

However, its long-term relevance will depend on its ability to evolve alongside its users, enhance educational value, and navigate regulatory complexities. As digital finance continues to grow, platforms like Fampay App India highlight the importance of designing systems that balance accessibility, safety, and usability for emerging user segments.